Global Market Outlook 2023

Wishing you a very happy and prosperous New Year 2023! It is that time of the year when we sit down and take stock of the year that passed and make necessary amendments with New Year resolutions for our life. This is no different for the markets either.

The year 2022 was a roller-coaster — soaring inflation, interest-rate hikes, recession risk in developed economies, and geopolitical shocks. Those who survived were disciplined, systematic, and diversified. This market outlook provides a broad, inter-market framework to navigate 2023.

Major Global Indices Performance CYTD

First, we will examine the performance of the major global indices year-to-date. The table above (if included) makes it clear that Indian markets have significantly outperformed major global benchmarks, and that trend may continue in 2023 despite macro headwinds.

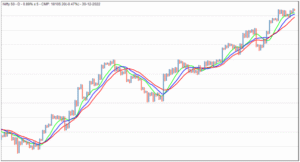

The Nifty 50 continued its rally, trading above key moving averages. That supports a sustainable uptrend (see Chart A below), though corrections are part of any bull cycle.

Having said that, market corrections are bound to happen even in the strongest bull cycles — they often shake out weak hands and are typically sharp but short-lived.

Chart B indicates divergence in the Nifty 50 price movement relative to momentum indicators — suggesting a reasonable probability of a correction. How deep and how long will depend on unfolding price action.

Sector selection will be important: watch PSU Banks, Capital Goods, Consumption and Automobile sectors for leadership rotations. Some decade-long leaders may underperform as cycles shift.

India VIX, often called the Fear Index, does not show major volatility spikes — instead it indicates subdued volatility and a gradual upmove as seen in Chart C below.

Gold Outlook

Turning to other asset classes — Gold is attractive. We see potential upside in the 18–20% range as Gold breaks out of consolidation (refer Chart D). Investors may maintain exposure to Gold for diversification and asymmetric potential returns.

USD/INR Outlook

Chart E shows USD/INR trading extended. The Rupee was Asia’s worst-performing currency in 2022 (≈ -11.5% vs USD). While a correction is possible, momentum suggests further USD strength in the near term. Targets near 85 and 89 are possible before any structural reversal.

Crude Oil Outlook

With COVID dynamics in China and slowing demand, Brent experienced a correction. Analysts expect demand recovery later in 2023 which could re-tighten the market.

Dow Jones Outlook

A medium-term view of the Dow shows extended zones (Chart F) and an elevated risk of correction. This doesn’t imply a long-term bear market, but calls for selective exposure and risk management.

Conclusion

The key takeaway: despite global slowdowns, India’s fundamentals remain relatively strong. With improving consumer sentiment, commodity trends, and policy tailwinds, Indian markets may outperform. Investors should stay diversified, maintain allocation discipline, and consider buying on meaningful dips.

Disclaimer: The views and suggestions are those of the author. This report is for private circulation and educational purposes only — not investment advice. Consult a licensed advisor for personal financial decisions.